401(k) vs Roth IRA vs Traditional IRA

401(k) vs Roth IRA vs Traditional IRA – Setting up a retirement plan should be easy enough. After all, you just want to make sure that you’ll live a good life after you retire.

However, the big world of retiring doesn’t come with easy to choose and understand options. Therefore, you may be faced with optimizing between a plain 401(k), a Roth IRA, and even with a traditional IRA option.

In this respect, we’re now going to talk about the aforementioned plans and tell you what to take into account when struggling to make a choice!

401(k)

This type of retirement plan is usually given to employees working for big companies. As a result, roughly 93% of employers offer their employees traditional 401(k) plans or others that are similar. When you pick a 401(k) option, money goes into a 401(k) account before it even reaches your paycheck. Therefore, as you extract it before it becomes a taxable income, so you enjoy a tax benefit in the present.

For example, if you’d make around $50k a year and save $5k in a 401(k), your taxable income would be lowered to $45k – thus, you will pay less in taxes, now. While 401(k) contributions are not taxed, the taxes are merely deferred to a later stage and the withdrawals from 401(k) are taxed.

401(k) Key Features

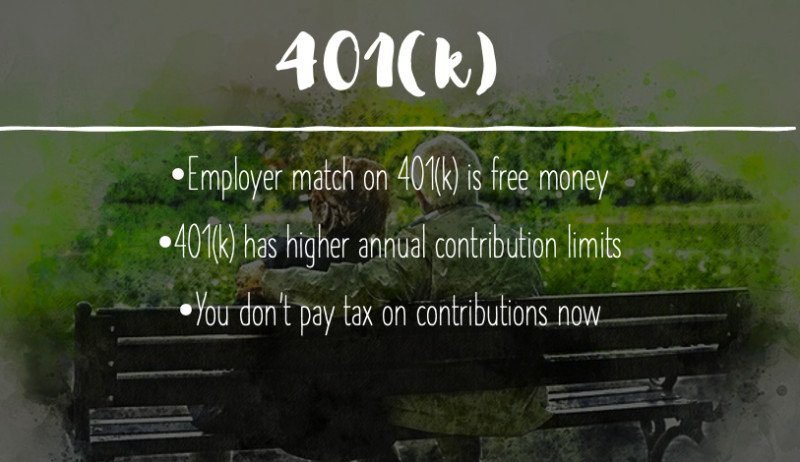

- Employer match is free money available to most employees. Employers match anywhere between 1-6% of annual income provided you are contributing the required amount as well.

- Tax-free contributions to 401(k) lowers the current tax liability, resulting in more net pay per paycheck.

- Tax liability is deferred to a later date, not waived

- 401(k) has higher annual contribution limits ($18,500) compared to IRA or Roth IRA

- Required minimum distributions – you are required to take money out when you reach the age of 70.5 years.

- The plan is maintained by employer and there is generally a smaller selection of funds available to invest in.

Avoid making these 401(k) mistakes.

Roth IRA

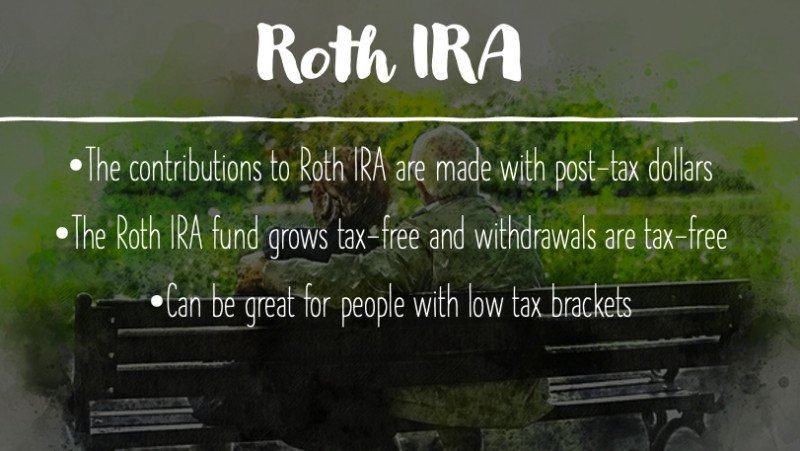

As you may know, a Roth IRA is an individual retirement plan that you can open with an investment firm or with a bank. Since this retirement strategy is not sponsored by an employer, anyone can open a Roth IRA. The main aspect of a Roth IRA is the fact that the contributions you make to it are taxable.

Roth IRA Key Features

- No minimum annual contribution requirement

- No age limitation for making contributions

- Funded with post-tax dollars, subject to an annual limit determined by IRS ($6,000 in 2020)

- Tax-free Growth of the fund

- Five year lock-in period i.e. you cannot withdraw until at least five years after the first contribution.

- Tax-free Withdrawal at retirement age

- No mandatory minimum required distribution at 70.5 years as in 401(k). You can let the fund grow further if you wish to.

- Early withdrawals are possible tax-free and penalty-free even under 59.5 years of age for qualifying reasons.

- Income earners above a cap ($139k in 2020, $140k in 2021 for single filers) are not eligible for Roth IRA contributions.

Traditional IRA

Lastly, for a traditional IRA option, the contributions made to it are usually tax-deductible, which reduces the taxable income with each year of contribution. Moreover, any investment earnings will not be taxed until you withdraw them from the IRA.

The main difference between a traditional and a Roth IRA is that the latter comes with fewer restrictions for the retired person and with more flexible early withdrawal rules.

401(k) vs Roth IRA – How to Decide?

It doesn’t matter when you want to retire – you have to start planning early!

There is no one-size-fits-all solution. For example, if you earn more than $139k (modified adjusted gross income) as an individual tax filer, then you are not eligible for a Roth IRA. On the other hand, a Roth IRA allows contributions of around $6k a year, while 401(k) plans allow you to contribute up to $19k per year (but investment choices would be limited as the plan is sponsored by the employer). Therefore, it really depends on how you want to carve out a strategy based on your investment style. You will have to assess your financial life, as well as your saving capabilities when choosing a retirement planning strategy. You will also have to keep yourself up to date with the yearly changes such as new restrictions, relaxations or the contribution limits.

Sample Allocation to 401(k) and Roth IRA

A sample strategy for allocating funds to 401(k) and Roth IRA could be the following:

Jane (single tax filer) earns $80,000 a year. She is eligible for making Roth IRA contributions and her employer offers her a 6% dollar-for-dollar contribution match on her 401(k).

Jane can contribute her portion (6% of $80,000 = $4,800) in 401(k) to get the employer match of $4,800. After that Jane can decide to contribute more to her 401(k) or put some money in Roth IRA. Jane believes that her post retirement tax-rates would be higher than her current tax-rates. She wants to tax advantage of the Roth IRA feature and pay lower taxes now and fund her Roth IRA account with $6,000.

After making contributions of $4,800 to 401(k) and $6,000 to Roth IRA, if Jane still wants to contribute to her retirement fund, she can choose to put some more money in her 401(k) account. She has still room to contribute $19,000 – $4,800 = $14,200.

This is just a sample strategy. In the end, you have to go with what works for you the best!

Read more

Popular Topics: Stocks, ETFs, Mutual Funds, Bitcoins, Alternative Investing, Dividends, Stock Options, Credit Cards

Posts by Category: Cash Flow | Credit Cards | Debt Management | General | Invest | Mini Blogs | Insurance & Risk Mgmt | Stock Market Today | Stock Options Trading | Technology

Useful Tools

Student Loan Payoff Calculator | Mortgage Payoff Calculator | CAGR Calculator | Reverse CAGR Calculator | NPV Calculator | IRR Calculator | SIP Calculator | Future Value of Annuity Calculator

Home | Blog

Page Contents